SINGAPORE INDUSTRIAL PROPERTY MARKET OVERVIEW

Based on Colliers International’s estimates, the majority 65.7% of the total pipeline warehouse supply is expected

to be located in the West planning region, followed by the East (20.1%), North (13.4%) and Northeast (0.9%)

planning regions.

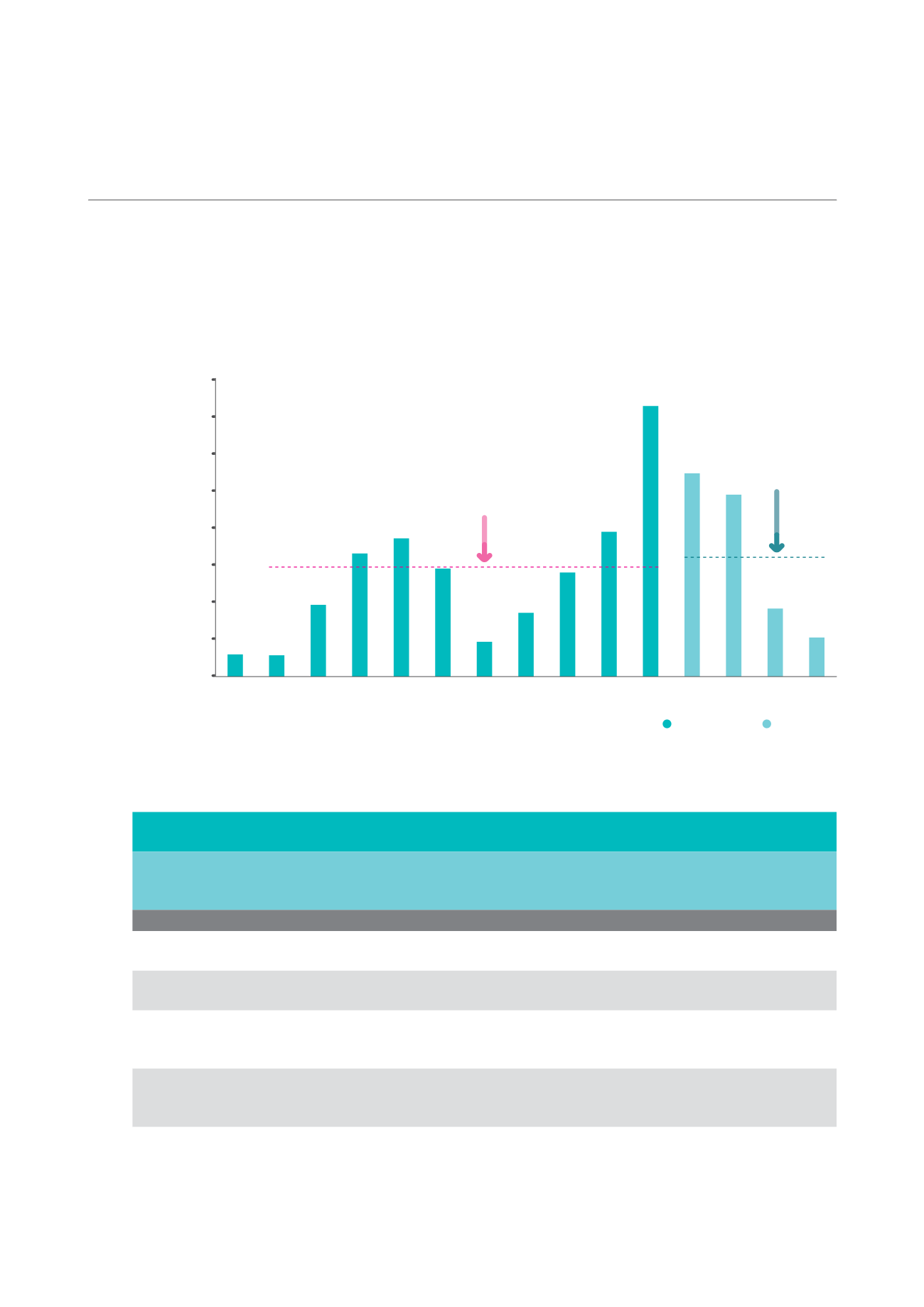

NET NEW AND POTENTIAL SUPPLY OF WAREHOUSE SPACE

(As of 4Q 2014)

F: Forecast

Source: JTC/Colliers International Singapore Research

2004

2008

2006

2010

2012

2005

2009

2007

2011

2013 2014

2018F

2015F 2016F 2017F

8,000

7,000

6,000

5,000

4,000

3,000

2,000

1,000

0

Net Floor Area ('000 sq ft)

Completed

Upcoming

Examples of major upcoming warehouse projects from 2015 to 2018 are provided in the following table.

Examples of Major* Known Potential Supply of Warehouse Space from 2015 to 2018

(As of 4Q 2014)

Project Name

Location

Developer

Estimated

Net Lettable

Area (sq ft)

Expected Year

of Completion

(TOP)

Single-User Warehouse

CWT Pandan

Logistics Centre

Pandan Avenue

CWT Project Logistics

Pte Ltd

606,793

2015

Warehouse

Buroh Lane

Warehouse Logistics Net

Asia Pte Ltd

613,236

2015

Warehouse

Jurong West Street 22 Tech-Link Storage

Engineering

(For LF Logistics)

847,915

2015

DHL Supply Chain

Advanced Regional

Centre

Greenwich Drive

HSBC Institutional Trust

Services (S) Ltd for Cache

Logistics Trust

928,100

2015

Singapore

Post Regional

eCommerce

Logistics Hub

Greenwich Drive/

Tampines Road

Singapore Post Limited 518,546

2016

10-year Average Annual

Net New Supply of

2.9 million sq ft from

2005 to 2014

Average Annual

Potential New Supply

of 3.3 million sq ft

from 2015 to 2018

continue on next page

CAMBRIDGE INDUSTRIAL TRUST | ANNUAL REPORT 2014

92