17 Due to the limitation on the type of sales caveat data/information recorded by the URA, analysis can only be carried out for multi-user factory space.

*Note that the average prices are dependent on the number and type of transactions that occur during the quarter/year. This in

turn depends on factors such as the location and age of the building as well as the floor level and size of the unit.

Source: URA REALIS/Colliers International Singapore Research

30-Yr Leasehold

Freehold/999-Yr Leasehold

60-Yr Leasehold

2004

2008

2006

2010

2012

2005

2009

2007

2011

2013 2014

4Q13 1Q14 2Q14 3Q14 4Q14

$0

$100

$200

$300

$400

$700

$500

$800

$600

$900

S$ per sq ft

Statistical Range of Monthly Rents of Islandwide Factory Space

Period

Minimum

(per sq ft)

25th Percentile

(per sq ft)

Median

(per sq ft)

75th Percentile

(per sq ft)

Maximum

(per sq ft)

Business Park

4Q 2013

S$3.15

S$4.00

S$4.49

S$5.25

S$8.70

1Q 2014

S$3.10

S$3.90

S$4.23

S$4.55

S$10.01

2Q 2014

S$2.99

S$3.80

S$4.16

S$4.36

S$6.40

3Q 2014

S$2.86

S$3.80

S$4.00

S$4.33

S$5.60

4Q 2014

S$3.00

S$3.80

S$4.09

S$4.31

S$6.10

Source: URA REALIS/Colliers International Singapore Research

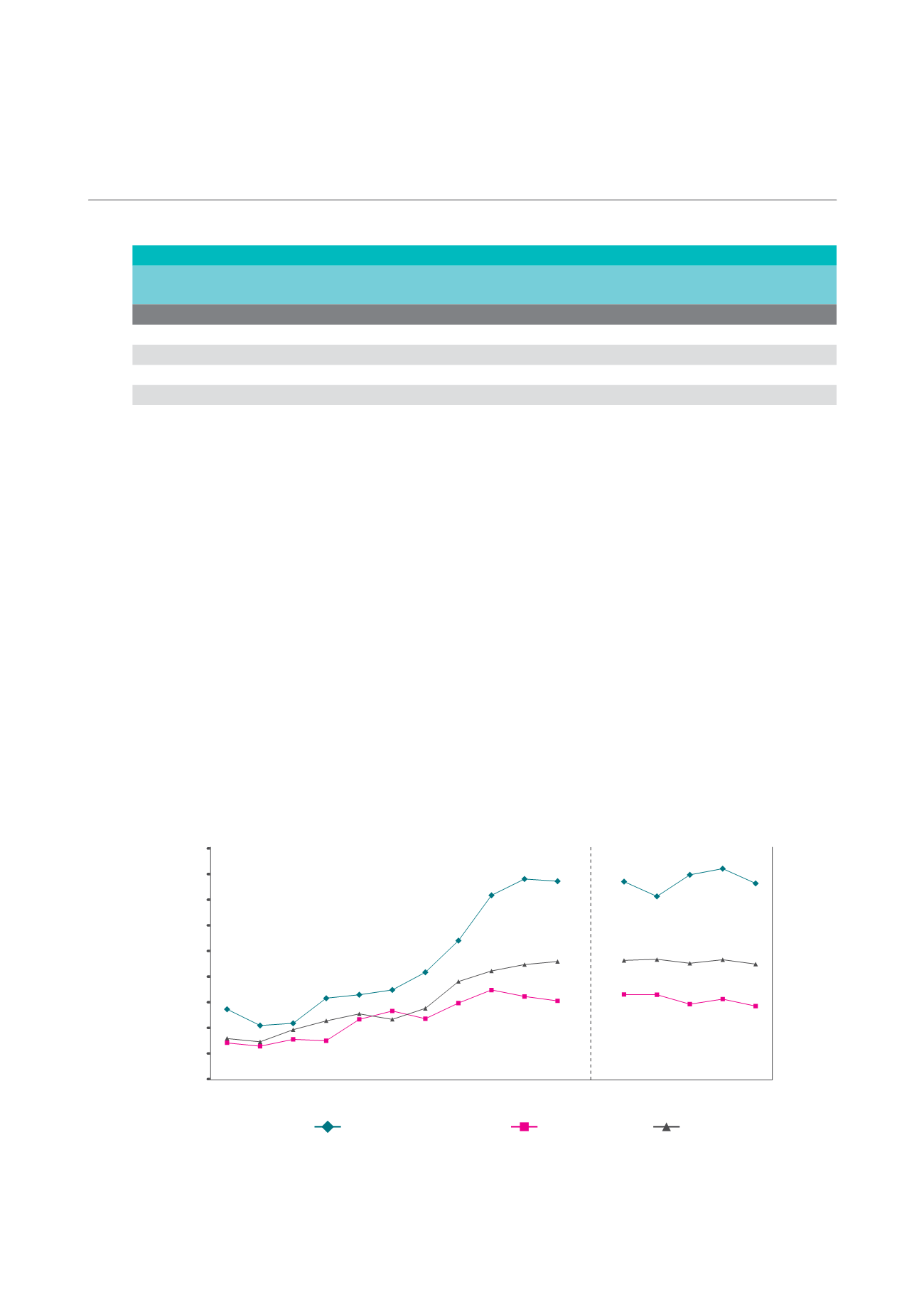

4.4 PRICE

Based on caveat records captured by URA’s REALIS as of 2 February 2015, average prices of 30-year leasehold

multi-user factory space

17

eased for the second consecutive year, by 5.3% YoY to S$307 per sq ft in 2014.

Conversely, prices of properties with longer tenure where supply is comparatively limited held up better. The

average prices of freehold/999-year leasehold multi-user factory space dipped 1.0% YoY in 2014, compared to

the 8.8% YoY rise in 2013, while average prices of 60-year leasehold multi-user factory space continued to rise

but at a slower pace of 2.7% YoY to S$460 per sq ft, compared to 2013’s 5.8% YoY gain.

This can be attributed to the slowdown in demand due to a price gap between buyers and sellers as well as the

continued effects of market measures such as the imposition of a SSD on industrial properties in January 2013

and the TDSR framework in late-June 2013. Additionally, the Government’s move to reduce the maximum tenure

of industrial sites sold under its IGLS programme from 60 to 30 years, and the ramped up IGLS programme in

recent years have resulted in stiffer competition among 30-year leasehold industrial properties, especially after

demand slowed down.

AVERAGE PRICES* OF FREEHOLD AND 30-YEAR AND 60-YEAR LEASEHOLD MULTI-USER FACTORY SPACE

CAMBRIDGE INDUSTRIAL TRUST | A WINNING FORMULA

89